Weekly Market Commentary – June 25, 2018

What time is it? The yield curve may be the pocket watch of economic indicators. It’s been around for a long time and it’s often right, but not always. The yield curve is the difference between the interest paid on two-year government bonds and 10-year government bonds. In normal circumstances, an investor would expect to earn a higher rate of interest when lending money to a government for 10 years than when lending money for two years because there is more risk associated with lending for a longer period of time. When the yield curve flattens or inverts, it suggests a shift in investors’ expectations. Financial Times explained: “The slope made up of bond yields of various maturities has a record of predicting recessions that would make even the savviest econometrician turn pea-green with envy. It is not perfect, but the curve has become flat and inverted – when short-term bond yields are actually higher than long-term ones – ahead of most economic downturns in most major countries since the second world war.”

In the United States last week, the difference between yields on 2-year Treasuries (2.56) and 10-year Treasuries (2.90) flattened. The gap narrowed to 34 basis points (a basis point is one-hundredth of one percent). The change reflects higher short-term rates, courtesy of the Federal Reserve. It also suggests tariffs and trade issues have made bond investors more pessimistic about prospects for U.S. growth, reported The Wall Street Journal.

Globally, the yield curve is inverted. “The average yield of bonds in JPMorgan’s broadest Government Bond Index that mature in seven to 10 years last week slipped below the average yields of bonds maturing in one to three years for the first time since 2007…that indicates that investors have a pretty grim view of where the world economy and equity markets are heading,” reported Financial Times. We’re keeping an eye on developments in the financial markets and will keep you informed.

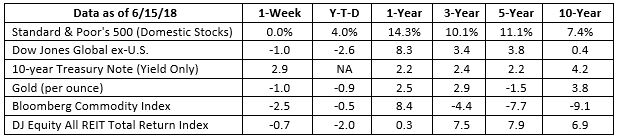

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT Total Return Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT Total Return Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

You knew carrots were good for your eyes, and a newly discovered use for the orange veggie may help farmers and/or food processing companies find a new source of revenue. That’s because carrots can make concrete stronger – and so do sugar beets. Engineers at Lancaster University in the United Kingdom are infusing nano platelets from discarded carrots and root vegetable peels into concrete. This strengthens the material in an environmentally friendly way. Durability + Design reported: “These vegetable-composite concretes were also found to out-perform all commercially available cement additives, such as graphene and carbon nanotubes and at a much lower cost…The root vegetable nano platelets work both to increase the amount of calcium silicate hydrate – the main substance that controls the performance of concrete – and stop any cracks that appear in the concrete.” The Economist reported adding 500 grams of platelets reduced the amount of cement required to make a cubic foot of concrete by 10 percent. In addition to reducing the amount of building material needed for a project, carrot concrete also reduces CO2 emissions.

Another natural material is getting a makeover, too. Researchers at the University of Maryland are refining processes that make wood stronger than steel, reported Scientific American. It may compete with titanium alloys and have applications beyond building: “A five-layer, plywood-like sandwich of densified wood stopped simulated bullets fired into the material – a result Hu and his colleagues suggest could lead to low-cost armor. The material does not protect quite as well as a Kevlar sheet of the same thickness, but it only costs about 5 percent as much, he notes.” If demand for carrots (and sugar beets and wood) increases and supply remains constant then we may see prices for those goods increase.

Weekly Focus – Think About It

“A person with a new idea is a crank until the idea succeeds.”

–Mark Twain, American author and humorist

Best regards,

John F. Reutemann, Jr., CLU, CFP®

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Investment advice offered through Research Financial Strategies, a registered investment advisor.

* This newsletter and commentary expressed should not be construed as investment advice.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the afternoon gold price as reported by the London Bullion Market Association. The gold price is set twice daily by the London Gold Fixing Company at 10:30 and 15:00 and is expressed in U.S. dollars per fine troy ounce.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Stock investing involves risk including loss of principal.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the Weekly Market Commentary please reply to this e-mail with “Unsubscribe” in

the subject.

Sources:

https://www.ft.com/content/49d0229e-73c7-11e8-aa31-31da4279a601

https://www.wsj.com/articles/trade-tensions-pinch-u-s-yield-curve-1529432210

https://www.durabilityanddesign.com/news/?fuseaction=view&id=19235