Market Commentary – December 17, 2018

Ouch!

It never feels good when the stock market heads south, and that’s what happened last week. The Standard & Poor’s 500 Index (S&P 500), Dow Jones Industrial Average, and Nasdaq Composite all moved into correction territory, which means the indices have fallen 10 percent or more from their previous peaks.

If you look at corporate earnings, the decline in U.S. stock values may seem a bit of a head scratcher. During the third quarter of 2018, almost four-fifths (78 percent) of companies in the S&P 500 were more profitable than analysts expected, according to FactSet Insight. Earnings grew by 25.9 percent – the fastest growth rate since 2010.

When you remember the stock market is a leading indicator, the mystery is resolved. Share prices reflect what investors expect will happen in the future, and third quarter earnings are in the past.

So, what moved the market last week? Investors’ concerns included slowing global economic growth. Dave Shellock of Financial Times reported:

“World equities closed out the week on a soft note as disappointing economic reports out of China and the eurozone heightened concern over the outlook for global growth…the big focus was on China, where activity and spending data confirmed that the country’s economy had a dismal November.”

Monetary policy and geopolitical issues, including the possibility of a U.S. government shutdown and ongoing Brexit follies, contributed to investor pessimism. The American Association of Individual Investors Sentiment Survey showed a 17-point decline in bullish sentiment and an 18.4-point increase in bearish sentiment.

When stock markets leave you feeling like Santa dropped coal in your stocking, it may be helpful to remember the words of Warren Buffett, “Be fearful when others are greedy and greedy when others are fearful.”

When the holidays are just too much. Around the holidays, it’s easy to become stressed and overwhelmed. Psychology Today offered some suggestions that may help you stay merry and bright, no matter what the season brings.

- Don’t lose sight of what makes you happy. It’s easy to become obsessed with everything being perfect. If you find yourself snapping because the shopper next to you got the last one, the holiday light display is sagging, or the table isn’t set just right, take a deep breath. True happiness often is found in everyday routines and healthy relationships.

- Give thanks for what you have. This seems like a natural corollary to point number one. Instead of focusing on what’s not quite right, redirect your thinking. Sure, your great aunt’s stories are inappropriate, and the mashed potato incident wasn’t great, but there are some good moments, too. If you can, find time to write down the things for which you are grateful to have in your life. Then, review it as needed.

- Do nice things for other people. Not everyone has a warm coat, much less a warm home and a patience-trying holiday meal. Giving to others can help give meaning to the season. You could donate to a favorite charity, help out at a food pantry or a shelter, or visit elderly neighbors. One of the very best aspects of giving is that it can make us happier.

- Embrace experiences. If you want to have a memorable holiday, don’t buy lots of gifts. Give experiences. Happiness research suggests, “…happiness is derived from experiences, not things…when they are shared, experiences allow us to get closer to others in a way impossible with inanimate objects that we can buy,” reported Paul Ratner on BigThink.com.

Weekly Focus – Think About It

“…in Racine, Wisconsin: The Santa at [the mall] knows sign language. He signs with kids who are hearing impaired, so that he can ask them – and they can tell him – what they want for Christmas. Because the warm fuzzy feelings of the holidays don’t just come from getting the right present – they come from feeling like part of a loving, inclusive community.”

–MentalFloss.com

Best regards,

John F. Reutemann, Jr., CLU, CFP®

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Investment advice offered through Research Financial Strategies, a registered investment advisor.

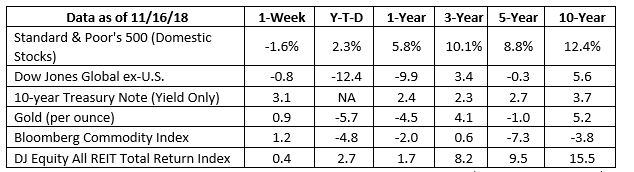

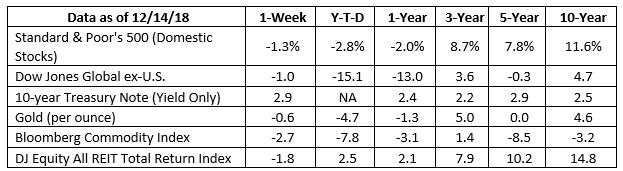

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT Total Return Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association.

Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

* This newsletter and commentary expressed should not be construed as investment advice.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the afternoon gold price as reported by the London Bullion Market Association. The gold price is set twice daily by the London Gold Fixing Company at 10:30 and 15:00 and is expressed in U.S. dollars per fine troy ounce.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Stock investing involves risk including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the Weekly Market Commentary please reply to this e-mail with “Unsubscribe” in the subject.

Sources:

https://finance.yahoo.com/news/u-stock-market-officially-correction-001801781.html

https://www.investopedia.com/terms/c/correction.asp

https://insight.factset.com/earnings-insight-q318-by-the-numbers-infographic

https://www.investopedia.com/articles/economics/08/leading-economic-indicators.asp

https://www.ft.com/content/cb5ddff4-ff45-11e8-ac00-57a2a826423e

https://www.ft.com/content/1d218d08-ffb5-11e8-aebf-99e208d3e521

https://www.aaii.com/sentimentsurvey

https://www.goodreads.com/quotes/29255-be-fearful-when-others-are-greedy-and-greedy-when-others

https://www.psychologytoday.com/us/blog/the-mindful-self-express/201412/how-find-peace-and-happiness-holiday-season

https://bigthink.com/paul-ratner/want-happiness-buy-experiences-not-more-stuff

http://mentalfloss.com/article/90086/20-heartwarming-stories-will-brighten-your-holiday-season