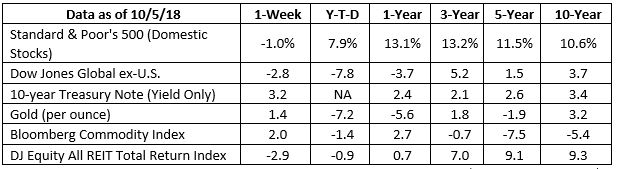

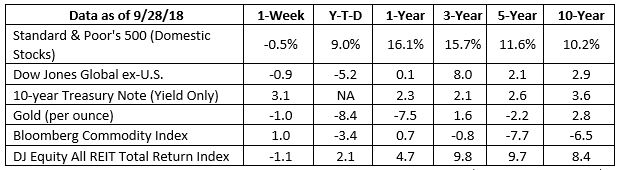

How rising interest rates are affecting the markets

It’s October, which means autumn is upon us. But this year, it’s not just the leaves that are falling. The markets have been falling, too. On Wednesday, October 10, the Dow slid more than 800 points. The S&P 500 fell for the fifth straight day. And the tech-heavy NASDAQ was hit hardest of all, dropping more than 4%.1 Both the Dow and the S&P continued sliding on Thursday, too.2

It sounds dramatic, but it’s not necessarily cause for alarm. Still, whenever market volatility rears its head, it’s useful to understand why. That’s because the more we understand the why, the less cause we have to fear it.

Before I delve into why, however, let me ask you a question. Do you remember the Greek myth of Theseus and the Minotaur? In the story, Theseus descends into a bewildering labyrinth to fight the half-man, half-bull Minotaur. But to find his way back, Theseus first ties one end of a ball of string to the entrance. Then, after slaying the beast, he follows the unwound string all the way back to the surface.

The reason I mention this story is because sometimes, navigating the markets can feel like wandering through an impenetrable labyrinth. There are so many headlines and narratives, each with their own twists and turns. The good news is that it’s possible to pick up a thread and follow it all the way back to its source, just like Theseus.

A ten-year journey

In this case, follow the thread back to the end of 2008. Seems like a long time ago, doesn’t it? Barack Obama had just been elected president. The academic paper that would lead to the creation of bitcoin had just been published. And people were just beginning to realize how bad the Great Recession would become.

To combat this, the Federal Reserve lowered the federal funds rate to almost zero.3 This is the interest rate that banks pay each other for overnight loans. Their reasoning was simple. By reducing the federal funds rate, banks could afford to lower their own interest rates to customers. Lower interest rates, of course, make it cheaper for businesses and individuals to borrow money, which spurs more investing and spending. This, in turn, could help revive America’s slumping economy. And with millions of jobs lost during the Great Recession, the economy needed all the help it could get.

Rates remained in the basement for years afterwards as the economy embarked on a long, slow healing process. In fact, it wasn’t until 2015 that the Fed finally raised rates at all.4

Now follow the string forward to 2018

The Fed has started lifting interest rates at a slightly faster pace in 2018. Recently, on September 26, the central bank announced they would raise the federal funds rate to a new range of 2.0 to 2.25%.5 Officials also suggested they might boost rates once more before the end of the year. It’s the third increase in 2018, and the eighth overall since 2015.

Why are interest rates going up? Because the economy is in a much stronger place!

Unfortunately, with that strength comes the risk of inflation. Inflation is the rate at which prices rise and purchasing power falls. For example, if the rate of inflation is 3%, then a candy bar that costs a dollar one year will cost $1.03 the next. It’s essentially the measure of how valuable your money is. And if inflation goes too high, it can make even basic living costs very expensive.

Historically, inflation goes up when interest rates are low. The Federal Reserve takes the risk of inflation very seriously. In fact, stabilizing inflation is one of the reasons the Fed was created in the first place. So, to prevent the economy from “overheating”, the Fed has slowly raised interest rates. This makes borrowing costlier and reduces spending, forcing the economy – and inflation – to grow at a slower rate.

Whew! Got all that? If so, congratulations! You’ve followed the string all the way back to the surface. We’ve finally reached the present day.

How higher interest rates affects the markets

There’s really no direct link between interest rates and the markets. The effect is more of the “ripple” variety. Despite this, higher interest rates tend to spook investors.

Remember, when the federal funds rate goes up, it costs more for banks to loan each other money. In response, banks raise their own interest rates. This makes borrowing more expensive for businesses and individuals, prompting them to cut back on spending. Less spending for businesses means less investment, less expansion – and less growth. And when investors think a company isn’t growing, they tend not to invest in that company. On the individual side, higher rates can also mean less disposable income for people to spend or invest.

There are other reasons why the markets are struggling. Falling bond prices (which are directly correlated with rising interest rates). Trade tensions between the U.S. and China. Like I said, the markets can be positively labyrinthine. But interest rates are one of the main drivers behind this sudden surge in volatility.

And now you know why.

So where do we go from here?

As important as interest rates are, they’re still just one thread. There are plenty of others that could cause the markets to rise or fall. For instance, a fresh bit of good economic news could transform this week’s fears into last week’s memories. And with the economy as strong as it is, would that really be a surprise?

This is why we don’t overreact whenever the markets lurch one way or the other. You see, when it comes to working toward your goals, we do everything possible not to fall into a labyrinth of twists, turns, and changes in direction. Instead, it’s better to keep things simple. To stay above ground. To follow our own path, not headlines or individual economic indicators.

In the story of Theseus and the Minotaur, Theseus was advised to “go forwards, always down, and never left or right” to reach his goal. The road to your goals isn’t quite so cut-and-dry. But the point is, Theseus had a plan. A strategy. And with the help of ball of string, he never deviated from it.

We also have a strategy: To diversify across a range of asset classes, choose fundamentally sound investments, and invest for the long term, not the short. And while you don’t have a ball of string, you have something even better: A team of experienced professionals dedicated to holding your hand while you work toward your goals.

It’s October. It’s a time for falling leaves, trick or treating, and an endless array of pumpkin flavored beverages. It’s not a time for stressing about the markets. So enjoy the season, remembering that here at Research Financial Strategies, we’ll keep watching Washington, Wall Street, and your portfolio. Every day, every week, every month, and every year. As always, please let us know if you have any questions or concerns. We’re always happy to talk to you! In the meantime, have a great month!

P.S. If you have any friends or family who are concerned about the markets, or don’t have a financial advisor to help them, please feel free to share this letter. Thanks!

Sources:

1 “Dow falls 832 points in third-worst day by points ever,” CNN Business, October 10, 2018. https://www.cnn.com/2018/10/10/investing/stock-market-today-techs-falling/index.html

2 “U.S. Stocks Seek Stability on Heels of Wednesday Rout,” The Wall Street Journal, October 11, 2018. https://www.wsj.com/articles/markets-tumble-across-asia-led-by-tech-as-growth-worries-dominate1539225820?mod=article_inline?mod=hp_lead_pos1

3 “Fed Cuts Key Rate to a Record Low,” The New York Times, December 16, 2008. https://www.nytimes.com/2008/12/17/business/economy/17fed.html

4 “Federal Reserve raises interest rates for second time in a decade,” The Washington Post, December 14, 2016. https://www.washingtonpost.com/news/wonk/wp/2016/12/14/federal-reserve-expected-to-announce-higher-interest-ratestoday/?noredirect=on&utm_term=.af1a4b1da520

5 “Fed Raises Interest Rates, Signals One More Increase This Year,” The Wall Street Journal, September 26, 2018. https://www.wsj.com/articles/fed-raises-interest-rates-signals-one-more-increase-this-year-1537984955