Let’s hear it for 2019!

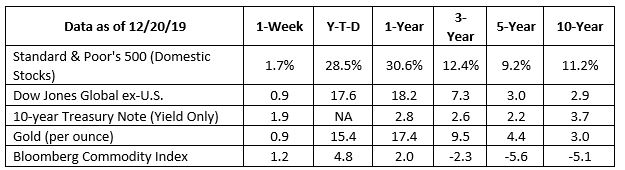

Major stock indices in the United States and overseas are poised to deliver double-digit gains for the year. Even with uncertainty about Britain’s exit from the European Union (EU), the FTSE 100 boasted a gain of more than 10 percent at the end of last week. That’s not bad for a year which included (in the United States) an inverted yield curve, an earnings recession, and a contentious trade war.

The strong stock market performance of 2019 owes a lot to central banks, and so does the performance of the bond market. Reuters reported, “…the screeching change of direction by the world’s top central banks, led by the Federal Reserve, which cut U.S. interest rates for the first time since the financial crisis more than a decade earlier…fired bond markets up like a rocket. U.S. Treasuries, the world’s benchmark government IOU, have made a whopping 9.4 percent after yields plunged as much as 120 basis points…German Bunds – Europe’s safest asset – have had their best year in five years, making roughly 5.5% in euro terms as the European Central Bank has reversed course too.”

So, what lessons should we take from 2019?

Perhaps, we should try to come to terms with loss aversion. When you make an investment decision, it’s important to consider the impact of loss aversion on your thinking. The pain from a loss carries twice the impact of the pleasure from a gain. As a result, fear of loss may affect investment decision making.

2019 offered a great example. During a year of exceptional returns, investors pulled money out of stocks at a record pace because they were worried about recession and other issues. Axios reported, “Data from the Investment Company Institute shows money has been pulled out of [stock investments] in every month this year except January. In total, more than $130 billion has been drawn from [stock investments] in 2019, making it already the largest year of outflows on record.”

When it comes to investing, uncertainty is normal. It is part of investing. Tolerating uncertainty may help investors earn attractive returns. As a result, our advice is to stay invested even when uncertainty makes you nervous, even when markets are falling.

If you have a diversified portfolio built to help you reach your goals, stay with it, unless you risk tolerance has changed. In 2019, pulling money out of stocks meant some investors missed out on some exceptional returns.

Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, MarketWatch, djindexes.com, London Bullion Market Association.

Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

The secure act may affect your retirement and your legacy planning

…Last week, reports indicated the ‘Setting Every Community Up for Retirement Enhancement’ (SECURE) Act was attached to the federal spending bill President Trump signed into law on Friday.

The SECURE Act is intended to expand retirement savings opportunities. Many of its provisions make it easier for Americans to save more for retirement and, also, to convert their savings into income for retirement. The Act will change IRA rules in some significant ways. For instance, Drinker Biddle and Barron’s reported:

- Contribute to IRA accounts at any age. In the past, Americans had to stop contributing to IRAs at age 70 ½.

- Begin taking required minimum distributions (RMDs) at age 72. The age for RMDs was pushed to 72 from age 70 ½.

The Act also changes post-death IRA distribution rules, eliminating stretch IRA estate planning strategies. Barron’s explained, “Under the bill, beneficiaries of an IRA would need to draw down the account – and pay income tax on the money – over a decade, rather than a lifetime.” This will affect some legacy planning strategies and necessitate the adoption of alternative solutions.

Workplace plans may change, too. Part-time workers are now eligible to participate in defined contribution plans as long as certain criteria are met. The Act also made it easier for defined contribution plans of all sizes to add lifetime income options to plan investment lineups.

In addition, the incentive for smaller business owners to establish workplace retirement plans increased. Tax credits, of up to $5,000 for three years, can be claimed to offset plan start-up costs. Additional tax credits are possible when new plans include automatic enrollment features or existing plans add automatic enrollment features.

If you would like to discuss how the SECURE Act may affect your retirement, business, or legacy plans, please give us a call.

Weekly Focus – Think About It

“I feel that one of the most important lessons that can be learned is that what we ‘see’ may be different than what is actually in front of us.”

–Mark Singer, Journalist [8]

Best regards,

John F. Reutemann, Jr., CLU, CFP®

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Investment advice offered through Research Financial Strategies, a registered investment advisor.

Most Popular Financial Stories

Words to Live By #1 – Perseverance

A major part of my job – perhaps the most important part – is helping people reach their financial goals in life. Over the course of my career, I’ve discovered...

* This newsletter and commentary expressed should not be construed as investment advice.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment. You cannot invest directly in an index.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the afternoon gold price as reported by the London Bullion Market Association. The gold price is set twice daily by the London Gold Fixing Company at 10:30 and 15:00 and is expressed in U.S. dollars per fine troy ounce.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* The Dow Jones Industrial Average (DJIA), commonly known as “The Dow,” is an index representing 30 stock of companies maintained and reviewed by the editors of The Wall Street Journal.

* The NASDAQ Composite is an unmanaged index of securities traded on the NASDAQ system.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* There is no guarantee a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

* Asset allocation does not ensure a profit or protect against a loss.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the Weekly Market Commentary please reply to this e-mail with “Unsubscribe” in the subject.

Sources:

https://www.barrons.com/market-data?mod=BOL_HAMNAV (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/12-23-19_Barrons_Market_Data.pdf)

https://www.barrons.com/articles/the-s-p-heading-for-best-year-since-2013-what-fueled-the-rally-51576891986?mod=hp_DAY_3 (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/12-23-19_The_S%26P_Is_Heading_for_Its_Best_Year_Since_2013.pdf )

https://www.reuters.com/article/us-global-markets-2019-graphic/the-best-year-financial-markets-have-ever-had-idUSKBN1YO266

https://thedecisionlab.com/biases/loss-aversion

https://www.axios.com/2019-record-cash-pulled-out-stocks-5d4763a9-5724-4c64-be23-356c4fcbd002.html

https://www.drinkerbiddle.com/insights/publications/2019/12/congress-finally-passes-the-secure-act

https://www.barrons.com/articles/navigating-the-secure-act-what-retirement-savers-need-to-know-to-optimize-their-401-k-s-and-iras-51576886142?mod=hp_LEAD_3 (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/12-23-19_Navigating_the_Secure_Act_What_Retirement_Savers_Need_To_Know_To_Otimize_Their_401ks_And_IRAS.pdf)

https://www.fool.com/retirement/general/2014/08/31/5-retirement-quotes-to-make-you-a-smarter-investor.aspx