No Results Found

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Many homeowners will form evacuation plans for their homes and practice them with family members, but most have failed to include their pets. An evacuation plan is a necessity for every home, especially if you live in an area where fires, and other disasters are a possibility. Take these steps to add your pets to your evacuation plan.

Assign pet evacuation responsibility to an adult.

Everyone in the household should know what to do during an evacuation. That includes assigning one parent or adult to the pets. This allows the other parent and the children to focus on their part of the evacuation plan, so there’s no confusion during a high-stress moment when time is of the essence.

Keep evacuation maps and pet carriers readily accessible.

If you need to evacuate, you should know exactly where every important item is located. If your pets require carriers, keep them in a place that you can access easily. Don’t forget any essential medications which might not be easily replaced in an emergency situation.

Practice your plan.

Include your pets in your home evacuation drills. It will help you see how they will respond and make changes to your evacuation plan if necessary. Getting your dog out of a window may not be as simple as you think!

Be prepared in case you get separated from your pets.

No matter how much you drill your evacuation plan, it’s possible that a dog or cat will run off while you’re focusing on keeping your family safe. A microchip or a GPS-compatible tag can help you find your pets once it’s safe to return to the area. Make sure all pets wear collars and tags with up-to-date identification information. Your pet’s ID tag should contain his name, telephone number and any urgent medical needs

Get a Rescue Alert Sticker

This easy-to-use sticker will let people know that pets are inside your home. Make sure it is visible to rescue workers (we recommend placing it on or near your front door), and that it includes the types and number of pets in your home as well as the name and number of your veterinarian. If you must evacuate with your pets, and if time allows, write “EVACUATED” across the stickers.

After months of relative quiet, the trade war between the U.S. and China has erupted again in a big way. The markets are the most immediate casualty, with the Dow plunging over 600 points on Monday alone.1

In all likelihood, you’re probably more focused on things like spring cleaning, your upcoming summer plans, and the end of Game of Thrones. My job in this letter is to briefly explain what’s going on, what matters, what doesn’t, and why you can go back to focusing on those other things

So, here’s what’s going on:

Failed deals lead to new tariffs

You may have noticed that headlines about the trade war had been rather muted in 2019. That’s because negotiators for both nations had been quietly working behind the scenes to come to an agreement on how to address the $375 billion trade deficit the U.S. has with China. The White House expressed optimism that a deal was close – until a sudden hardening of positions prompted both sides to retreat to their corners.

On Friday, May 10, President Trump raised the stakes by placing 25% tariffs on all Chinese imports that had previously been spared. Here’s how the U.S. trade representative put it:

“[The President has]…ordered us to begin the process of raising tariffs on essentially all remaining imports from China, which are valued at approximately $300 billion.”2

Throughout this trade war, it has seemed like both countries are waiting for the other to blink first. Both are still waiting. For on Monday, May 13, China announced it would raise tariffs on $60 billion in U.S. goods, some up to as much as 25%.3

Why all this matters to the markets

You’ve heard, of course, of the principle of cause and effect. If one thing happens, something else is affected. Fail to brush your teeth and you get cavities. Leave meat out of the refrigerator too long and it will spoil. You get the idea.

Investors, analysts, money managers, and traders who participate in the markets on a daily basis make decisions based on cause and effect. How tariffs impact certain companies is a perfect example of this. For instance, imagine a fictional American company called Widgets n’ Stuff, or WNS for short. In order to make its widgets, WNS buys thingamajigs from China. But thanks to tariffs, the price of importing thingamajigs goes up.

Investors know this, and thanks to the principle of cause and effect, predict it will have a negative impact on WNS’s finances. Maybe they’ll have to raise prices on their own widgets to make up the difference. Maybe they’ll have to produce fewer widgets. You get the idea. So, investors sell stock in Widgets n’ Stuff because it no longer looks like an attractive investment.

Like them or not, tariffs act as a double-edged sword that affect companies and consumers on both sides of the Pacific. On the American side, China’s tariffs can make it harder for U.S. companies to sell their goods to Chinese consumers. At the same time, American tariffs can make it harder for U.S. companies to import the goods they need for their own products. Either way, prices go up, corporate finances suffer, and consumers are often the ones left to foot the bill. That’s why the markets care about the trade war.

But here’s why all this doesn’t matter to us – yet

The principle of cause and effect is important, but it’s more important to short-term traders than long-term investors like us. That’s because we don’t actually know what the long-term effects are yet. We can guess, but guessing isn’t really a viable strategy in life, is it?

Think of it this way. Let’s say you come down with a fever. The short-term effect is that you probably don’t feel very good. But the long-term effect isn’t yet known. Perhaps it’s just a symptom of a mild cold that will pass in a few days – and that’s why we don’t immediately start chugging antibiotics the moment we feel sick.

While it’s never fun, the markets have fallen after almost every round of tariffs to date. Each time, the markets absorbed the blow, and then rebounded relatively quickly. Previous trade war battles faded into the background and investors turned their attention to other things. Will that happen again this time? We don’t know. And that’s the point: We don’t know what the long-term effects are. What’s more, with the markets having enjoyed a remarkable bull market in recent years, we can afford to be patient. What we can’t afford is to make important decisions by guessing at the long-term effects of these tariffs.

Hippocrates once wrote that, “To do nothing is sometimes the best remedy.” For that reason, it’s okay for you to go back to planning your summer vacation or betting which character will die next on Game of Thrones. In the meantime, my team and I will continue monitoring all the causes and effects in the markets. If, at some point, we have a better understanding of the long-term effects of this trade war, we’ll make decisions accordingly.

As always, please let us know if you have any questions or concerns. We are always happy to speak to you!

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

1 “Dow plunges 700 points after China retaliates with higher tariffs,” CNN Business, May 13, 2019. https://www.cnn.com/2019/05/13/investing/dow-stocks-today/index.html

2 “Trump Renews Trade War as China Talks End Without a Deal,” The NY Times, May 10, 2019. https://www.nytimes.com/2019/05/10/us/politics/trump-china-trade.html?module=inline

3 “After China Hits Back With Tariffs, Trump Says He’ll Meet With Xi,” The Wall Street Journal, May 13, 2019. https://www.wsj.com/articles/china-to-raise-tariffs-on-certain-u-s-imports-11557750380

“We are now in a bear market – here’s what that means.” – CNBC headline on December 24, 20181

“The stock market rally to start 2019 is one for the history books.” – CNBC headline on February 22, 20192

If you’re like most people, it’s probably not uncommon for you to plan your day or week based on the weather forecast. For example, you might check the forecast, see that it’s supposed to be sunny, and decide to go fishing on Saturday.

But when Saturday rolls around, it starts to rain.

The frustration you’d feel is very similar to how investors and analysts often feel about the markets. The forecast says one thing – and then the opposite happens.

For example, let’s go back to the end of 2018. For months, the markets had been hammered by volatility. The Nasdaq entered bear market territory. Many pundits predicted even more volatility after the new year.

But four months later, the markets are on the verge of record highs.

So, the question is: Why the change in direction? What’s behind this year’s market rally? And most importantly, what can we learn from it?

The volatility that dominated the end of 2018 was largely due to fears of an economic slowdown. The Federal Reserve raised interest rates, which can cool both inflation and economic growth. Trade tensions with China showed no signs of stopping. Corporate earnings slowed down, oil prices had dropped, and several other indicators had many analysts predicting a recession in 2020 or 2021.

Even after the turn of the year, there was some interesting data that, when compared with historical trends, suggested more storms on the horizon. For example, you may have seen the term “inverted yield curve” bandied about in the media for a time. We’re venturing into “financial nerd” territory here, but this is when the yield on short-term Treasury bonds rises higher than the yield on long-term bonds. It doesn’t happen often, and historically, it has sometimes been a sign of an impending recession. The result of all these signals was a forecast that had many investors reaching for their umbrellas, convinced that gloomy weather was here to stay.

But instead, the markets enjoyed their strongest start to a year since 1998.3

In many ways, this rally has been driven by something very simple: Nothing really got worse. The Federal Reserve has stopped raising interest rates, saying that it won’t raise them again in 2019.4 The trade war with China seems to have hit a lull. And now, investors can point to a host of different historical trends that work in their favor. For example, some data suggests that when the stock market rises 13% or more “during the first three months of a calendar year,” it will gain even more before the end of the year.3

So, does that mean the good times are here to stay?

No.

Warren Buffett, the legendary investor, has a saying: “Be fearful when others are greedy and greedy when others are fearful.” While we shouldn’t take that maxim too literally, it does illustrate an important point. Time after time, conditions that cause fear can change in an instant, leaving the fearful behind. On the other hand, conditions that stoke greed can shift before you know it, giving the greedy a nasty shock.

On their website, CNN has something called the Fear & Greed Index. 5 Using seven different indicators, they can calculate which emotion is driving the markets most at any given time. As of this writing, that emotion is greed. A few months ago, it was fear. As we’ve just seen, the scale can swing from end to another very quickly.

When you look more closely at the data, there are still reasons to think a recession is possible in the next year or two. (A contracting labor market, problems in Europe, stocks being valued too highly, to name just a few.) Other data suggests that the stock market’s current highs are overblown.6 But does this mean it’s time to run and hide? Nope! While data is very good at telling us what was and what is, it’s still unreliable at telling us what will be – at least as far as the markets are concerned. In fact, for as much grief as we give meteorologists for getting a forecast wrong, they do a much better job predicting the weather than experts do the markets!

Here’s what we can learn from all this

As your financial advisor, the reason I’m sending you this letter is because there are a few things I think we need to keep in mind as 2019 rolls on.

First, we need to remember to guard against recency bias. Recency bias is when people make the mistake of thinking what happened recently is what happens usually. It’s why investors tend to panic during market volatility or take on unnecessary risk during a market rally.

Second, remember that emotion is a good servant, but a bad master. Emotion helps us interact with other people. It makes experiences more memorable and life more colorful. But it can be come harmful if it drives our decisions. We should always strive to keep our own personal Fear & Greed Index from swinging too sharply one way or the other.

Finally, whether the markets go up, down, or sideways, you’ll probably hear about many different statistics, indicators, and historical trends that predict this, that, or the other thing. When you do, remember that correlation is not causation.

Correlation, as you probably know, is the measurement of how closely related two things are. In finance, we often find that many things tend to change in sync with one another. Asset classes, market sectors, you name it. It’s why we spend so much time looking at things like inverted yield curves – because they are often correlated with the health of the markets or economy.

But just because two things are correlated does not mean that one causes the other. (It’s why an inverted yield curve doesn’t always mean a recession is nigh.) All the indicators and historical trends you hear about in the news are important, and worth studying – but again, they only tell us what was or what is. Not what will be.

So, to sum up:

• Just as we didn’t give in to fear when the markets were down, so too will we not give in to greed while the markets are up.

• We will remember that sun today doesn’t protect against rain tomorrow, or vice versa.

Instead, we’ll make decisions as we’ve always done: by keeping your long-term goals foremost in our minds. In other words, we’re not working to help you go fishing just this weekend.

We’re working to help you go fishing any weekend you want.

As always, if you have any questions or concerns about the markets, please don’t hesitate to contact us. In the meantime, have a wonderful Spring!

1 “We are now in a bear market – here’s what that means,” CNBC, December 24, 2018. https://www.cnbc.com/2018/12/24/whats-a-bear-market-and-how-long-do-they-usually-last-.html

2 “The stock market rally is one for the history books,” CNBC, February 22, 2019. https://www.cnbc.com/2019/02/22/the-stockmarket-rally-to-start-2019-is-one-for-the-history-books.html

3 “The Stock Market is Having Its Strongest Start in 21 Years,” Money, March 20, 2019. http://money.com/money/5639032/stock-market-strong-start/

4 “Fed holds line on rates, says no more hikes ahead this year,” CNBC, March 20, 2019. https://www.cnbc.com/2019/03/20/fedleaves-rates-unchanged.html

5 “Fear and Greed Index,” CNN Money, accessed April 17, 2019. https://money.cnn.com/data/fear-and-greed/

6 “Dow, S&P 500 and Nasdaq near records but stock-market volumes are the lowest in months,” MarketWatch, April 18, 2019. https://www.marketwatch.com/story/why-stock-market-volumes-are-the-lowest-in-months-as-the-dow-sp-500-and-nasdaq-testrecords-2019-04-17

If your portfolio lost more than 10% in the last recession, you need to take another look at how you are managing risk.

Jim Streight James Streight Chief Marketing Officer

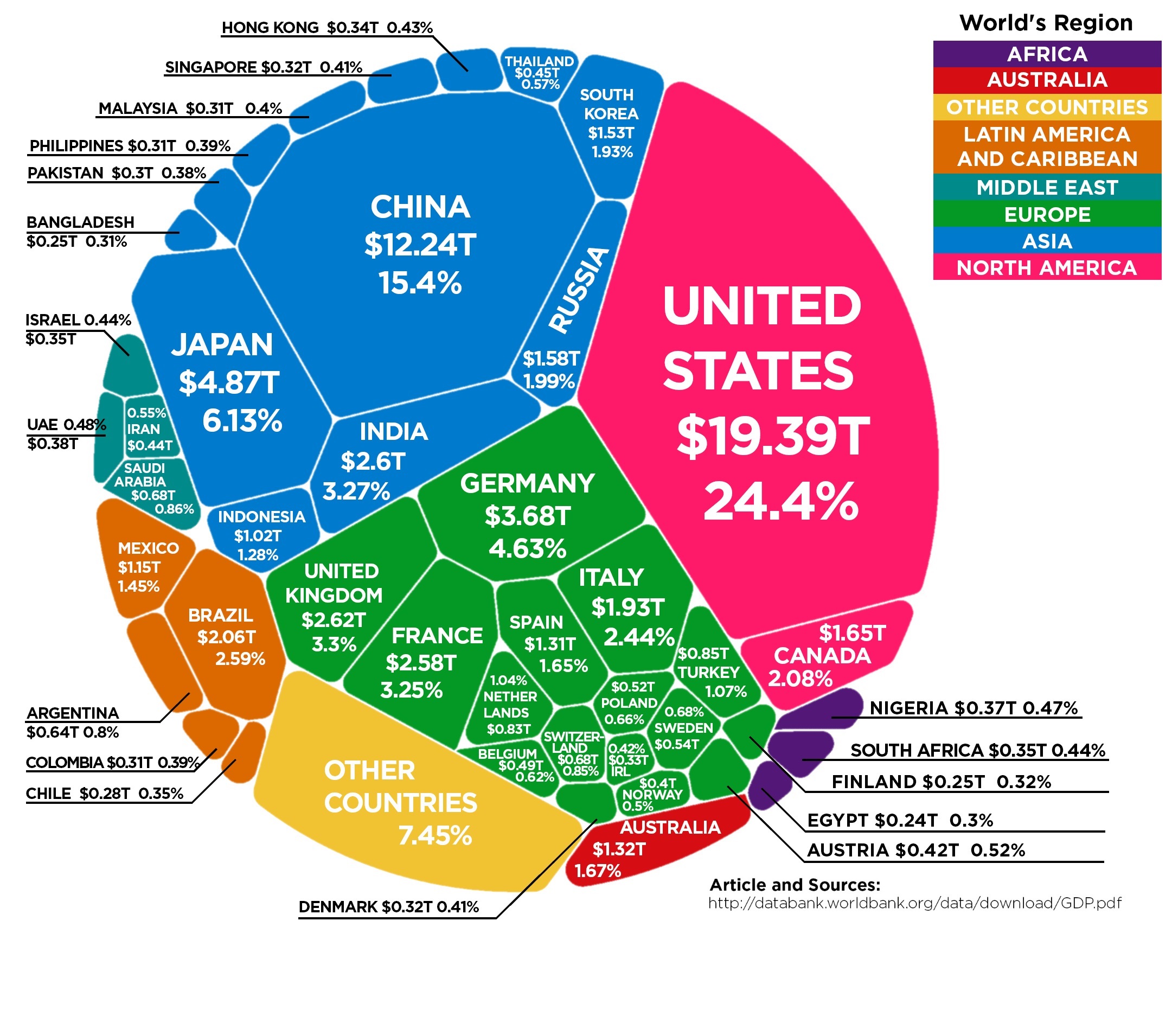

Open any newspaper or tune in to your favorite news channel and you will find much talk about how China is taking over the world’s economy. They have made incredible strides in building infrastructure, manufacturing and their military during the past few decades. In fact, there’s so much talk today about their incredible growth rate and the power of their economy; we may forget just how good we are doing in the United States.

The magnitude of what they have accomplished in such a short period of time is amazing. They’ve literally flooded millions of people from their rural hometowns with the Three Gorges project and forced them to move to the cities. They are relocating 250 million people, according to a NY Times report, from the countryside to the city, from farms to factories.

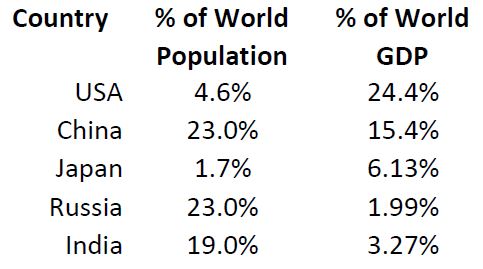

Whether it’s a national news channel or an every day American, many believe that our country’s best days are behind us. One easy way to understand if the economic growth of the USA is healthy is to examine our GDP vs. world GDP. GDP = Gross Domestic Product. It’s the total of all the goods and services each country provides to the world economy. The table below with data from World Bank has some statistics for comparison:

When we examine the graphic, the USA is in the top spot generating 24.4% of world GDP with 4.6% of the world population. China is number 2 producing 15.4% of world GDP with 23% of the world’s population. Those numbers are worth reading again!

The USA is still way ahead of other countries! We are 80% smaller than China, yet we are almost double their GDP.

A strong economy brings great wealth. The rule of law and personal property rights are two of the most basic principles of a capitalistic economy. The USA maintains both.. Not so much in China. Hence, the emerging problem in China. The Chinese can create excessive amounts of wealth and then what? Many leave China and they take their wealth with them. That is because at the end of their life someone in the Chinese government is just going to take it. But in the USA, it is different. Your cars, investments, homes and possessions. You get to determine the final distribution of your possessions. That’s personal property rights and the rule of law protecting you. Two totally different philosophies!

Examining the table further, Japan is the third largest economy. Remember what everyone said about Japan in the late 80’s? Japan was faster and more nimble than the USA. Well, their economy peaked in 1989 at 13.9% of the world’s GDP. Currently, Japan produces 6.13% of the world’s GDP.

India and Russia both have a large population and are nuclear powers. Combines they have 42% of world population. Yet, combined at 5.26% GDP, they do not even exceed Japan!

Recently, India’s economy is growing enormously. They also have personal property rights similar to the USA. They maintain the rule of law and are the world’s largest democracy. India has been working industriously to grow their economy. If there’s one country on this list who has the potential sometime in the future to better the US in GDP, it’s most likely India.

The Russians have always been on everybody’s radar. A significant amount of their GDP involves energy production but their growth has all but stagnated.

This is a lot of information to consider. The USA is the most productive country on Earth. No other country is even close. China has had a 1000 year head start on us. (How come we don’t hear about this on the news every night!)

The constant talk of a trade war and tariff’s is overblown. Many people believe it won’t affect the USA much in the long run. We have had tariffs for years. Our trading partners had tariffs against us which were usually higher. For example, we held a 2.5% tariff on German cars being imported into the US but paid 10% on US vehicle entering into Germany. Very lopsided and ignored by our politicians for a long time. We’ve had trade wars before. We survived because we are very resilient and the rest of the world relies on our productivity. A trade war and tariff’s will hurt the Chinese economy much greater and my guess is they will eventually come to the table and negotiate a fair deal for everyone.

We are in a very strong negotiating position in the USA. Our people have always been driven by independence, innovation, and the pursuit to do better. We attract some of the greatest talent of the world to increase our productivity and lead the way in industry after industry.

Final thought: The United States of America isn’t going to relinquish our top GDP title anytime soon. Someday it may happen- maybe it will be India- but it will be a long time from today.

Stocks were mixed last week as fresh economic data points and election-related uncertainty slowed market momentum. The Standard & Poor’s 500 Index fell 0.96 percent, while the Nasdaq Composite Index rose 0.16 percent. The Dow Jones Industrial Average dropped 2.68...

Stocks posted modest gains last week, with quarterly earnings season in full swing and the election on the horizon. The Standard & Poor’s 500 Index increased 0.85 percent, while the Nasdaq Composite Index rose 0.80 percent. The Dow Jones Industrial Average...

Stocks advanced last week despite mixed inflation data, lurching oil prices, and lingering anxiety about the Middle East. The Standard & Poor’s 500 Index gained 1.11 percent, while the Nasdaq Composite rose 1.13 percent. The Dow Jones Industrial Average picked up...

Stocks were essentially unchanged last week as geopolitical tensions added some volatility to an otherwise quiet trading week. The Dow Jones Industrial Average was flat (+0.09 percent), while the Standard & Poor’s 500 Index ticked up 0.22 percent. The Nasdaq...

Stocks moved higher last week, continuing to build on the momentum generated after the Federal Reserve decided to cut short-term rates by 0.50 percent. The Standard & Poor’s 500 Index gained 0.59 percent, while the Nasdaq Composite rose 0.95 percent. The Dow Jones...

When you hear “hot dog” and “inflation” in the same sentence, you might think of those supermarket franks that plump up when cooked. In this case, we’re talking about the original dogs of the ballpark, a cultural touchstone of America’s pastime. The average price of a...

The page you requested could not be found. Try refining your search, or use the navigation above to locate the post.

Everything we do starts with learning what is important to you. Understanding your unique story is vital in the development of a plan with your best interests in mind. Connect with us to learn more.

Our focus is on your life and priorities. Not just your portfolio. That’s why we start by listening and learning about you. Each individual client has different needs and concerns that need to be addressed. And because we carefully listening to those concerns, we will gain important information that will help us to best serve our clients and help protect their financial futures.

Together we will work to implement the plan that was developed for you. We will keep you constantly updated on what is happening and evolve our plan as your life happens.

Above all, our advisors want to help you meet your goals, even if that means helping you find out what your goals are.

We are here for you whenever you need us. Call your Research Financial Strategies Financial Advisor at any time, for any reason. You will always have access to the guidance you need whether it is high tech, high touch or a combination of the two. Your personal Financial Advisor will help you figure out how to pay for life’s great adventures!

Historically low interest rates present a welcome opportunity for many homeowners to improve their financial situation by refinancing their mortgage. But, like everything else in the world of finance, there are no free lunches. To take advantage of these lower rates, homeowners must leap the FICO hurdle.

To qualify for the best loans at the lowest rates, borrowers must qualify financially and are scored by lenders using a computerized model for evaluating credit risk, developed by Fair, Isaac, and Company, known as the FICO score.

Mortgage lenders are in the business of making money by lending it and being repaid on time. They gauge the risks associated with making that loan on a number of factors, not the least of which is the likelihood of timely repayment.

The FICO scoring system compares borrower’s credit capabilities to those of similar borrowers all over the country. A borrower’s credit history gives a strong indication of integrity, attitude, and discipline as well as a measure of their capability to pay bills on time.

Three major credit reporting agencies gather credit information: Experian, Equifax, and Transunion. The firms act independently of each other and use different methods for gathering information, hence the reports of each may differ.

The reporting agencies issue several different types of reports. A Consumer Report is the basic consumer report issued when an individual orders his own credit report. The Merchant Report is more complete and contains the full FICO scores.

Lenders view these scores as just one of several criteria for evaluating the ability of a borrower to pay back a loan. The scores, ranging from 0 to 850, are numbers that tell lenders how likely an individual is to repay a loan, or make credit payments on time. The higher the score, the better the credit risk. Scores of 700+ make A credit grades, 640+ for a B grade, and below 579 fail.

According to mortgage broker Ron Goerss of Partners Mortgage, the most important factors to mortgage lenders are mortgage history, derogatory credit history, liens or judgments, length of credit history, depth of credit history, proportion of debt to credit balances, and the amount of available credit.

A borrower can improve his FICO score over time by paying bills—especially mortgage payments—on time. Late payments cost points. To get the best scores, one should accumulate at least 36 months of a timely payment history. Generally speaking, a borrower will have an excellent credit score with four major accounts ($1,500 credit limits or higher) all with 36 months of spotless payment history, and all usually maintaining balances that are at or below 60% of available credit limits.

Despite paying bills on time, it is still possible to have a lower credit score. Too many open accounts with higher balances will pull the score down. Too many inquiries hurt the score. Too many monthly obligations weaken the score.

Finally, the real negatives are late mortgage payments, collection history, charge-offs, repossessions, and bankruptcy. While all of those can be worked around, most lenders will refuse a conventional loan to someone with foreclosure history on their report.

It’s a good idea to periodically review your FICO score. Erroneous information may be reported, and if you know ahead of time, you can write a letter to the credit-reporting agency and request a correction. For more information on FICO scoring and obtaining your FICO scores: www.creditline.com and www.creditreporting.com.

We all know it is inevitable. It’s no secret healthcare costs will be going up. For years, medical expenses have been steadily increasing. In 2007, medical expenses rose almost 12 percent. However, the rate of increase slowed to 6 percent during the past five years and that trend is expected to continue for the foreseeable future, according to a June 2018 report from PwC. While single-digit increases can be considered an improvement, ever-rising costs are a concern for those who have to foot the bill, today and in the future.1

Medical expenses are often the “elephant in the room” in a retirement plan. It’s the expense people prefer not to consider because, if they do, they’ll need to save significantly more money.

How much should you save for healthcare in retirement?

According to the Fidelity Retiree Health Care Cost Estimate, the average 65-year-old couple that retired in 2018 should have had about $280,000 set aside for medical expenses in retirement, excluding long-term care. The estimate assumes the couple does not have employer-provided retiree healthcare coverage, and does qualify for Medicare.2

Fidelity anticipates retirees’ healthcare savings may be spent like this:2, 3

Strategies for managing retirement healthcare costs

Whether you plan to retire in five, 10, or 20 years, there are a few things you can do to better prepare for healthcare in retirement:

1. Do the math. Fidelity’s estimate is an average. Your healthcare situation is unique, so it is a good idea to create a more personalized estimate, one that includes the cost of various premiums and insurance costs, as well as prescription medicines.4

2. Get the skinny on discounts. No matter how old you are, your doctor and your pharmacist can provide valuable suggestions about how to reduce prescription drug costs. Don’t hesitate to ask about coupons or discounts that could lower your costs. Pharmaceutical companies may have coupons available through their websites. Also, investigate other options such as substituting a generic drug, using a mail-order prescription service, or filling a 90-day supply instead of a 30-day option. Even small savings can add up over time.5, 6

3. Open a Health Savings Account (HSA). Your employer’s high-deductible health plan (HDHP) comes with a useful option – a health savings account (HSA). You can save for current and future medical expenses in an HSA, and they confer a triple tax advantage

If you don’t spend the money in your HSA, you can roll it over to the next year. Also, the account is yours, even if you change employers. As a result, HSAs are a great way to save for healthcare costs in retirement.7

Healthcare costs are likely to be a significant part of your retirement budget. If you haven’t already factored these costs into your retirement plan, you may want to consider it. The sooner you prepare, the better off you will be.

Please contact us if you want to discuss your options. We’re happy to help.

Sources:

1 https://www.pwc.com/us/en/health-industries/health-research-institute/assets/pdf/hri-behind-the-numbers-2019.pdf

2 https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

3 https://medicare.com/coverage/how-much-of-all-my-health-care-costs-does-medicare-cover/

4 https://www.thebalance.com/how-to-plan-for-health-care-costs-in-retirement-2388478

5 https://www.medicare.gov/drug-coverage-part-d/costs-for-medicare-drug-coverage/costs-in-the-coverage-gap/6-ways-to-lower-drug-costs

6 https://finance.yahoo.com/news/14-ways-survive-rising-healthcare-100300296.html

7 https://money.usnews.com/money/retirement/aging/articles/2018-10-17/6-myths-about-hsas-for-retirement

8 https://news.gallup.com/poll/234302/snapshot-americans-project-average-retirement-age.aspx

9 https://www.ssa.gov/OACT/quickcalc/early_late.html

10 https://www.ssa.gov/planners/retire/delayret.html

11 https://money.usnews.com/money/retirement/medicare/articles/2018-03-21/9-ways-to-reduce-health-care-costs-in-retirement